Since 40 years, IAEA develops and maintains a comprehensive database focused on nuclear power plants worldwide, namely PRIS (Power Reactor Information System). We have collected and analysed data starting from 2005 up to date. You can find here below shown in 5 graphs some information on new power reactors connected to the grid, those under construction, those being decommissioned on schedule, or those retired in advance.

We have not taken into account the Japanese reactors not in permanent shutdown. Since Fukushima accident and the following ban on NPP operations, 4 Japanese NPP have restarted. All of these between last summer and a few days ago. We have considered the remaining ones – not yet restarted neither yet in permanent shutdown – in a sort of Limbo: in fact, they are operable, but still waiting for the authorities and politicians’ starting signal.

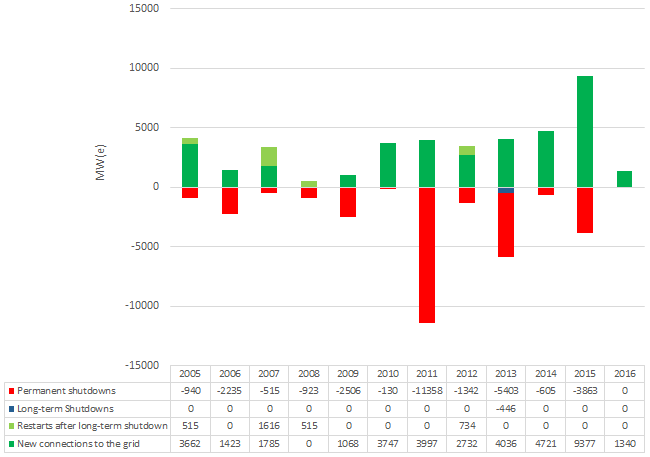

As can be seen in Figure 1, the new installed nuclear power from January 2005 to January 2016 amounts to 37,9 GWe, a value which exceeds the reduced capacity from permanent shutdowns by 8,1 GWe.

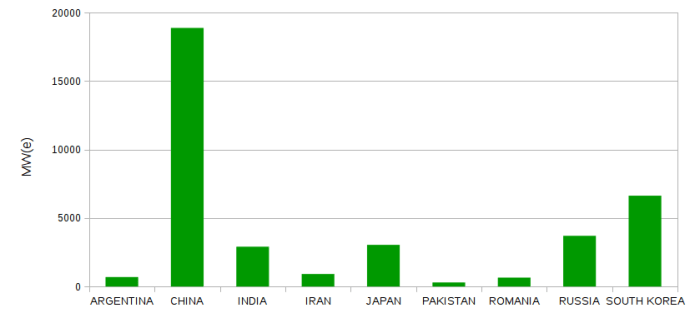

Let’s consider the state-by-state contribution to the new installed reactors (Figure 2). China remarkably drives overall NPP replacement with roughly 18 GWe of new capacity connected to the grid, and with an average construction duration just above 5 years. In the same time frame, South Korea follows it by return, with an average schedule duration just below 6 years.

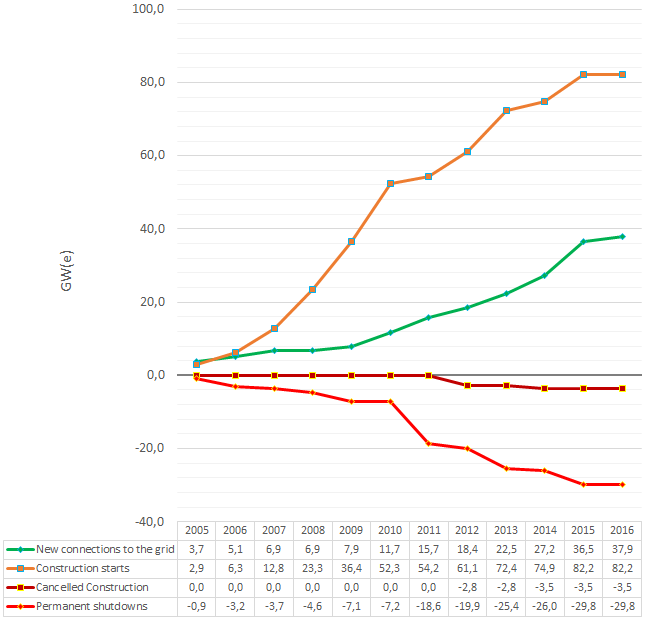

By analyzing the year-by-year progress (Figure 3), two notable aspects deserve our attention. First of all, we observe a significant drop of installed nuclear capacity in 2011, mainly as a direct or indirect consequence of the Japanese 11th March earthquake and tsunami: among the thirteen permanent shutdowns in that year, four are from the site of Fukushima Daiichi, while eight are from German power plants which have been forced to early retire due to the political decision to accelerate the country’s nuclear phase-out.

The second interesting aspect is the outstanding amount of new capacity connected to the grid in 2015, which doubled the results of the previous year.

What could we expect for the near future? Is the 2015’s achievement just a flash in the pan, or can we say that it is the restart of the nuclear renaissance?

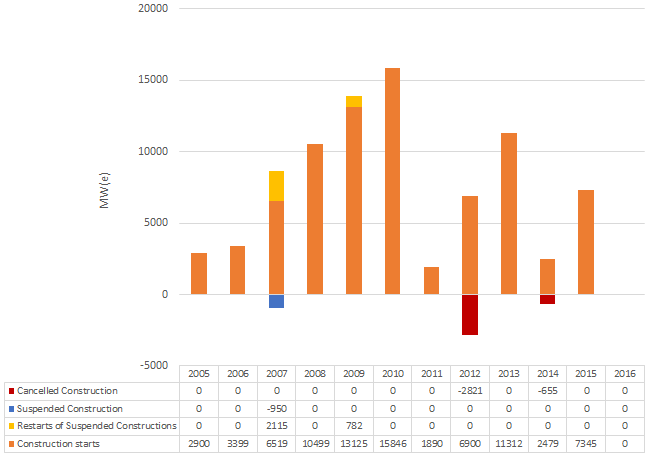

To answer the question we ought to look at the amount construction starts in the last ten years. As can be seen in Figure 4, in four years from 2007 to 2010 the construction of nuclear power plants has experienced tremendous growth. After that, in some ways all construction plans have suffered from the impact of the Fukushima accident. However, there is a bunch of eleven Chinese reactors still under construction, starting from 2009-2010. So, taking into account the average duration of NPP construction in China – very short time, as per performances consolidated over the past ten years – as well as the number of reactors which are about to be completed in India, Japan, Pakistan, Russia, South Korea, UAE and USA, for the next two years we expect results equal to those for the last, or even more.

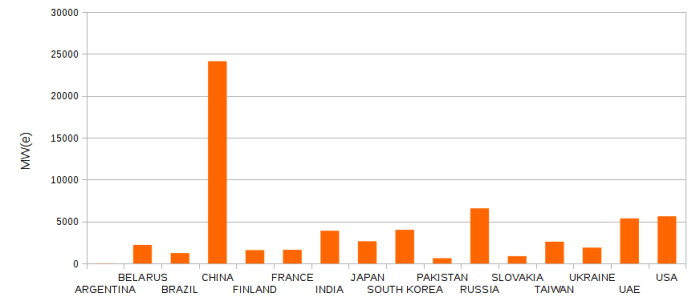

Figure 5 shows the state-by-state summary of the total capacity for all nuclear reactors under construction, as of January 2016.

In short, the race to nuclear power plants is currently destined to take place primarily on the racetracks of the Far East (from 2016 to 2020, six to eight nuclear reactors will probably be approved each year in China). And this despite the current slowdown in economic growth – also felt over there. The situation is made even more interesting by the fact that the countries chasing China are almost exclusively the emerging ones – some of these are “in the early days of development”.

Nothing new on the western front? Actually something is moving. Even if we are forced to admit that all factors against are dominant, at the moment. And perhaps it is time to fully review the role of nuclear power production in modernized countries, paving definitely the way for advanced nuclear systems – not necessarily always large. But that’s another story, about which we will not dwell here. That’s all folks, for now.